Executive Summary: The "Last Mile" of Cash

In the distribution and field sales ecosystem, selling is only half the job. Collecting the money is the harder half.

For decades, the "Collection Leg" has been dominated by two inefficient instruments: Cash and Cheques. Both are slow. Both are risky. Both create massive reconciliation headaches for the finance team back at the Head Office.

With the rise of UPI (Unified Payments Interface) in India, businesses have tried to modernize. Sales reps now carry laminated QR codes (Static QRs) or ask customers to "GPay to this number."

This creates a new problem: The Mystery Credit.

Your bank statement shows a credit of ₹4,530 from "Rakesh Kumar." You have 50 customers named Rakesh. Which invoice did he pay? Is it a part-payment? Is it an advance?

This blog post introduces the Intelligent QR Code—a dynamic, transaction-amount & invoice specific payment instrument that bridges the gap between the field interaction and your Tally ledger. We analyze how embedding intelligence into the payment layer can reduce your Days Sales Outstanding (DSO) by 30% and eliminate reconciliation drudgery.

1. The Problem: "Digital Money, Analog Reconciliation"

The friction in B2B collections isn't the transfer of money; it is the identification of money.

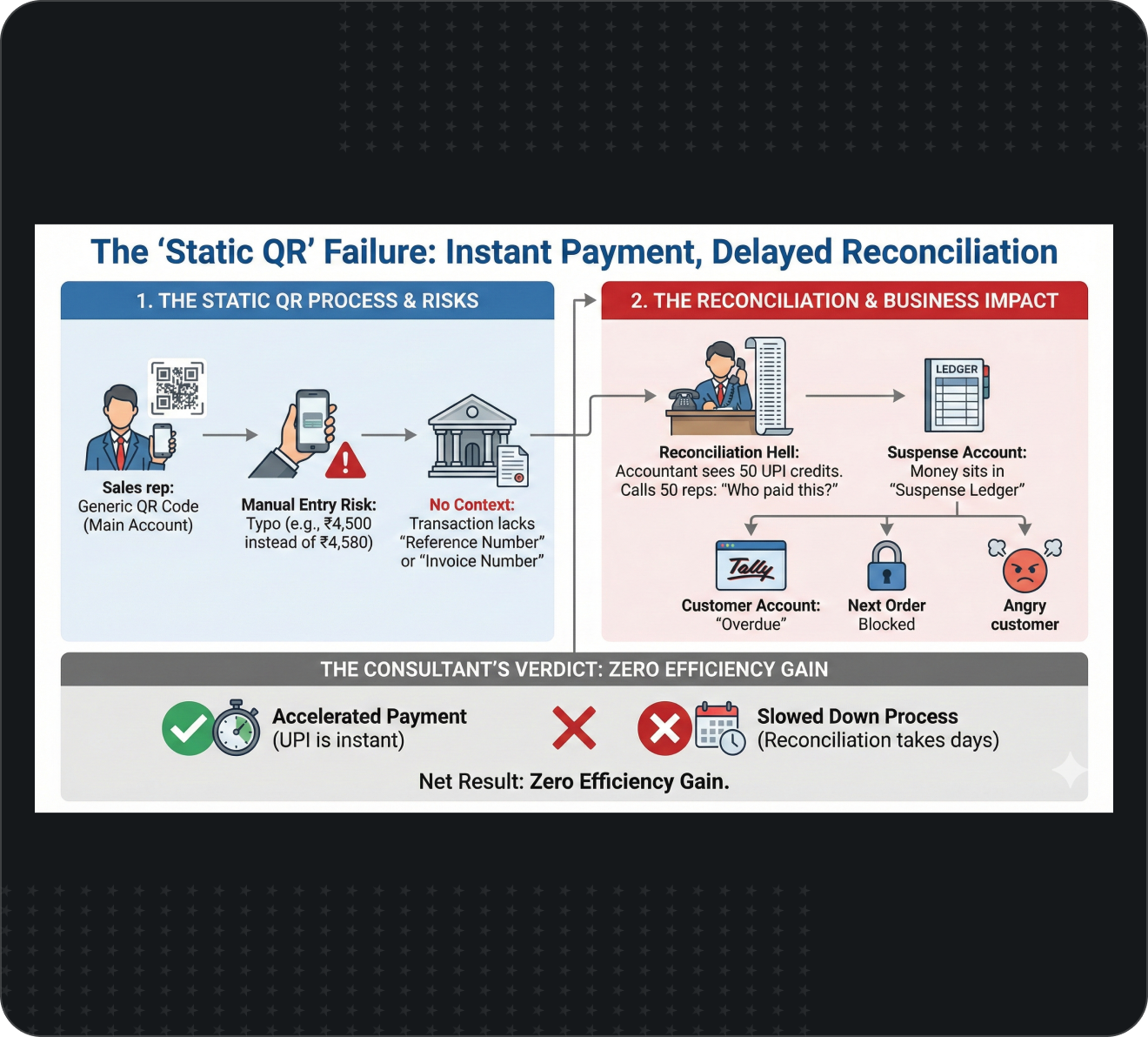

The "Static QR" Failure:

When a sales rep shows a generic QR code (the one linked to the company's main account) to a retailer:

Manual Entry: The retailer has to type the amount. (Risk: Typo. He pays ₹4,500 instead of ₹4,580).

No Context: The bank transaction carries no "Reference Number" or "Invoice Number."

The Reconciliation Hell: The next morning, your accountant downloads the bank statement. He sees 50 UPI credits. He has to call 50 sales reps to ask: "Who paid this ₹4,500?"

The Suspense Account: Until identified, the money sits in a "Suspense Ledger." The customer's account in Tally still shows "Overdue." The next order gets blocked. The customer gets angry.

The Consultant’s Verdict:

You accelerated the payment (UPI is instant), but you slowed down the process (Reconciliation takes days). Net result: Zero efficiency gain.

2. The Solution: The Intelligent (Dynamic) QR Code

An Intelligent QR Code is not a generic image. It is a piece of code generated in real-time for a specific transaction.

How Effortless Generates It:

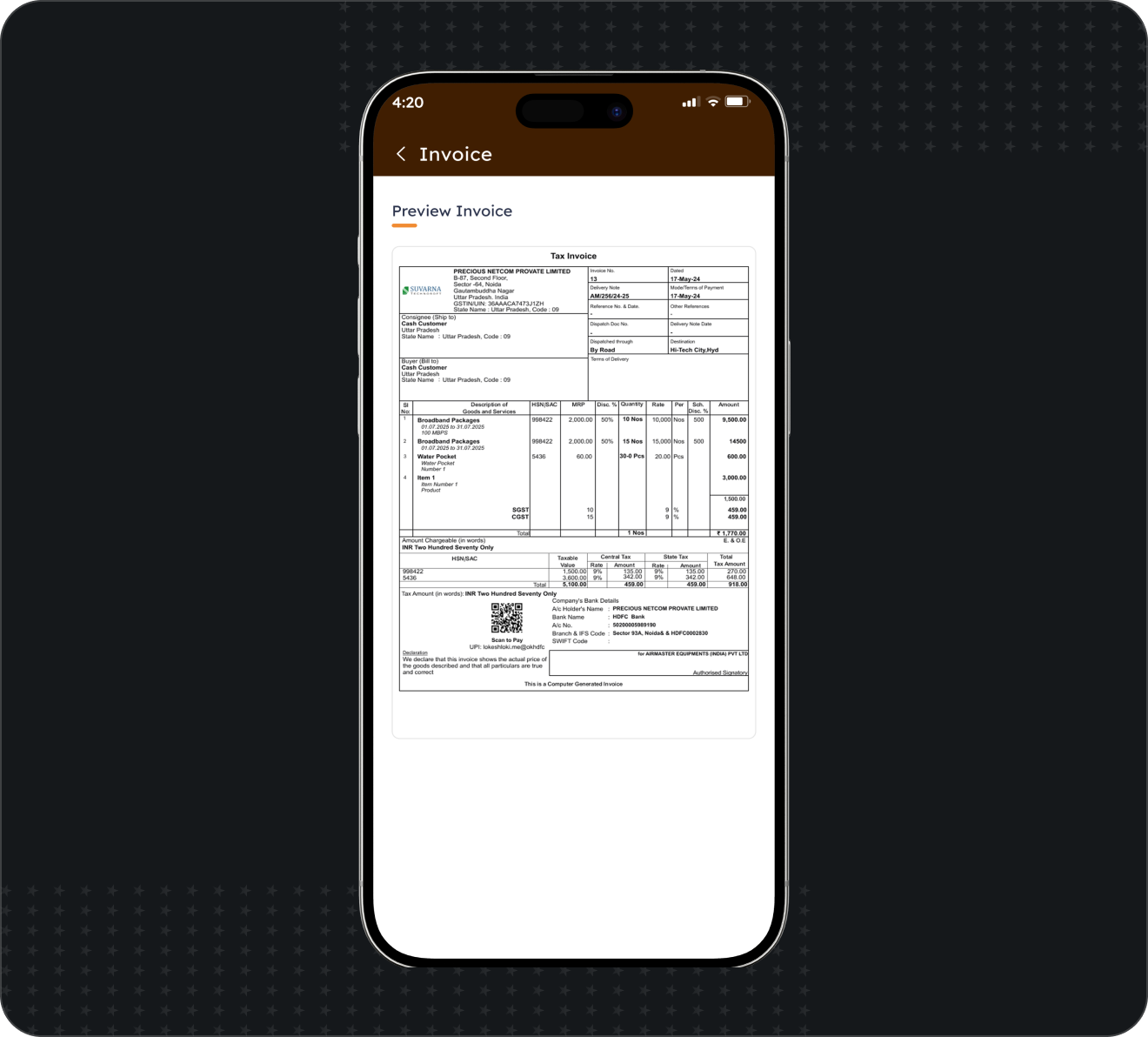

When your sales rep creates an sales order or invoice on the mobile order-taking app, the system generates a unique QR code embedded directly on the sales order or invoice PDF or the app screen.

The "Intelligence" Inside:

This QR code carries three locked data points:

The Exact Amount: The retailer cannot type ₹4,500. If the bill is ₹4,580, the QR locks the payment to ₹4,580.

The Beneficiary: It ensures the money goes to your official account, not the sales rep’s personal wallet.

The Reference ID (The Magic Key): It embeds the Invoice Number (e.g., INV-2026-005) into the transaction metadata.

3. The Workflow: From Scan to Tally in 3 Seconds

Let’s trace the journey of an Intelligent QR payment using Effortless.

Step 1: The Field Interaction

Action: The sales rep delivers the goods. He opens the payment collection app India module in Effortless.

Display: He clicks "Collect Payment." The app shows a QR code on his screen for Invoice #101.

The Scan: The retailer scans it using any UPI app (PhonePe, Google Pay, Paytm).

The Payment: The amount is pre-filled. The retailer enters their PIN. Payment Successful.

Step 2: The Instant Confirmation

Notification: The sales rep gets a "Success" tick on his app instantly.

Proof: He doesn't need to take a screenshot. The system records the Transaction ID automatically.

Step 3: The "Zero-Touch" Reconciliation

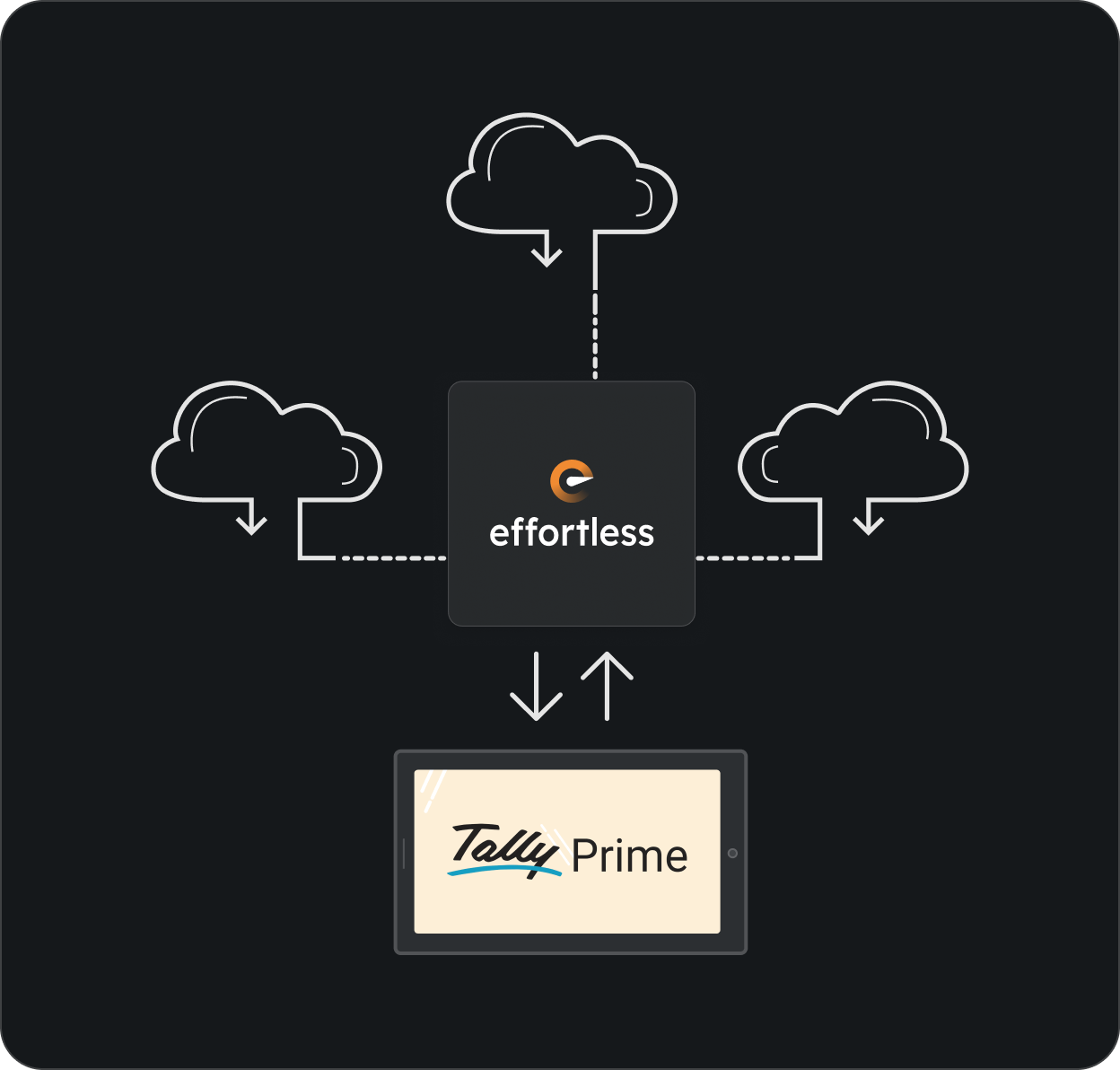

The Bank Sync: Effortless connects to your corporate bank account API.

The Match: It detects the incoming credit. It reads the Reference ID (Invoice #101).

The Tally Post: It automatically creates a Receipt Voucher in Tally.

Debit: Bank Ledger.

Credit: Customer Ledger.

Adjustment: Against Ref Invoice #101.

The Result:

The money is in the bank. The entry is in Tally. The customer's credit limit is freed. All within 5 seconds. No accountant touched a keyboard.

4. Strategic Impact: Killing the "Float"

Why does this matter for a ₹100 Cr company?

Because of Float.

In the "Cheque Economy," the float is 3-5 days (Collection -> Deposit -> Clearance).

In the "Static QR Economy," the float is operational (Money is in the bank, but the ledger is not updated for 2 days).

With Intelligent QR:

Float = Zero.

Re-Rotation of Capital: You can use that cash immediately.

Credit Limit Cycling: Because the customer’s ledger is updated instantly, they can place a new order immediately. You can rotate the same credit limit 4 times a month instead of 2. This doubles your sales velocity without increasing risk.

5. Beyond the Field: Intelligent "Payment Links"

This technology isn't limited to face-to-face sales. It solves the Remote Collection problem too.

The WhatsApp Scenario:

You have 500 small retailers who send orders via phone. You dispatch the goods. Now you need to collect.

Old Way: You call them. They say "sending cheque."

Effortless Way: How to send automatic payment reminders to customers on WhatsApp?

The system detects the invoice is due.

It generates a Payment Link (which is just a URL version of the Intelligent QR).

It sends a WhatsApp: "Dear Customer, Invoice #105 for ₹10,000 is due. Click here to pay."

Customer clicks -> UPI App opens -> Pays.

Tally auto-reconciles.

This transforms your "Accounts Receivable" department from a call center into an automated engine.

6. Conclusion: Stop Guessing, Start Knowing

The era of "Mystery Credits" must end.

In 2026, your finance team should not be playing detective with bank statements.

By deploying Intelligent QR Codes via Effortless, you achieve the holy grail of finance: Certainty.

Certainty of Amount.

Certainty of Source.

Certainty of Accounting.

Don't just digitize the money. Digitize the context.

Key Takeaways & FAQ

Q1: Do I need a specific bank account for Intelligent QR?

A: Effortless work with your UPI handle. Put it inside effortless centrally, it will auto generates QR basis transactions each time. We overlay the intelligence on top of your existing banking rails.

Q2: What happens if the customer pays a partial amount?

A: Intelligent QRs can be configured. You can choose to "Lock" the amount (Customer must pay full) or allow "Partial Pay" (Customer can edit amount). If partial payment is made, Effortless posts the receipt and leaves the remaining balance as "Outstanding" in Tally automatically.

Q3: Is there a transaction fee (MDR) on these payments?

A: For UPI transactions, there is typically zero or negligible cost (unlike Credit Cards which charge ~2%). This makes it cheaper than the cost of handling cash (risk of theft, counting time).

Q4: Can I use this for Van Sales?

A: Yes. This is perfect for field sales / street selling. The sales rep generates the invoice and the QR code on the spot. The money is collected before the rep leaves the shop, eliminating the risk of bad debt in Van Sales.

Q5: How to automate bank reconciliation with Tally using this?

A: That is the core feature. Because every QR code is linked to a specific Invoice ID, the Effortless reconciliation engine matches the incoming bank feed entry to the Tally invoice with 100% accuracy, creating the Receipt Voucher without human intervention.

Suggested Reading from the Effortless Edge Blog

The "Blind Spot" Audit: 5 operational metrics you cannot see in your Tally Profit & Loss – Why un-reconciled cash hides your true position.

E-Invoicing on the Go: Generating IRN/QR codes from the field – The first step of the digital invoice.

Stop Asking "Where is the Order?": The Case for Real-Time Field Visibility

Tired of asking "Who paid this?"

[Book a Collection Demo] and see the Intelligent QR in action.